MESOP’S MUST READ ! -Turkish financial crisis adds to region’s chaos

by David P. Goldman – Asia Times – February 5, 2014

More than coincidence accounts for the visit to Iran by Turkish Prime Minister Recep Tayyip Erdogan on January 28, the same day that his economic policy collapsed in a most humiliating way. As the Turkish lira collapsed to levels that threatened to bankrupt many Turkish companies, the country’s central bank raised interest rates, ignoring Erdogan’s longstanding pledge to keep interest rates low and his almost-daily denunciation of an “interest rate lobby” that sought to bring down the Turkish economy. Erdogan’s prestige was founded on Turkey’s supposed economic miracle.

Hailed as”the next superpower” by John Feffer of the Institute for Policy Studies, and as “Europe’s BRIC” by The Economist, Turkey has become the Sick Man of the Middle East. It now appears as a stock character in the comic-opera of Third World economics: a corrupt dictatorship that bought popularity through debt accumulation and cronyism, and now is suffering the same kind of economic hangover that hit Latin America during the 1980s.

That is not how Erdogan sees the matter, to be sure: for months he has denounced the “interest rate lobby”. Writes the Hurriyet Daily News columnist Emre Deliveli, “He did not specify who the members of this lobby were, so I had to resort to pro-government newspapers. According to articles in a daily owned by the conglomerate where the PM’s son-in-law is CEO, the lobby is a coalition of Jewish financiers associated with both Opus Dei and Illuminati. It seems the two sworn enemies have put aside their differences to ruin Turkey.”

US President Barack Obama told an interviewer in 2012 that Erdogan was one of his five closest overseas friends, on par with the leaders of Britain, Germany, South Korea and India. Full disclosure: as the Jewish banker who has been most aggressive in forecasting Turkey’s crisis during the past two years, I have had no contact with Opus Dei on this matter, much less the mythical Illuminati.

Erdogan was always a loose cannon. Now he has become unmoored. Paranoia is endemic in Turkish politics because so much of it is founded on conspiracy. The expression “paranoid Turk” is a pleonasm. Islamist followers of the self-styled prophet Fetullah Gulen infiltrated the security services and helped Erdogan jail some of the country’s top military commanders on dubious allegations of a coup plot. Last August a Turkish court sentenced some 275 alleged members of the “Ergenekon” coup plot, including dozens of military officers, journalists, and secular leaders of civil society.

Now Gulen has broken with Erdogan and his security apparatus has uncovered massive documentation of corruption in the Erdogan administration. Erdogan is firing police and security officials as fast as they arrest his cronies.

There is a world difference, though, between a prosperous paranoid and an impecunious one. Turkey cannot fund its enormous current borrowing needs without offering interest rates so high that they will pop the construction-and-consumer bubble that masqueraded for a Turkish economic miracle during the past few years.

The conspiracy of international bankers, Opus Dei and Illuminati that rages in Erdogan’s Anatolian imagination has triumphed, and the aggrieved prime minister will not go quietly. As Erdogan abhors old allies who in his imagined betrayed him and seeks new ones, the situation will get worse.

One of the worst ideas that ever occurred to Western planners was the hope that Turkey would provide a pillar of stability in an otherwise chaotic region, a prosperous Muslim democracy that would set an example to anti-authoritarian movements. The opposite has occurred: Erdogan’s Turkey is not a source of stability but a spoiler allied to the most destructive and anti-Western forces in the region.

It seems unlikely that the central bank’s belated rate increase will forestall further devaluation of the lira. With inflation at 7.4% and rising, the central bank’s 10% reference rate offers only a modest premium above the inflation rate. About two-fifths of Turkey’s corporate debt is denominated in foreign currency, and the lira’s decline translates into higher debt service costs. Turkey is likely to get the worst of both worlds, namely higher local interest rate and a weaker currency.

Source: Turkish Central Bank Source: Turkish Central Bank |

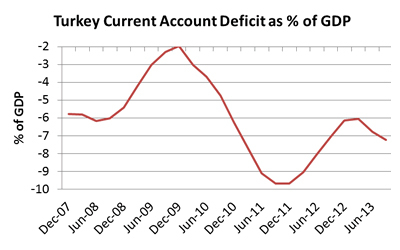

Now Erdogan’s Cave of Wonders has sunk back into the sand. Few analysts asked how Turkey managed to sustain a current account deficit that ranged between 8% and 10% of gross domestic product during the past three years, as bad as the Greek deficit during the years before its financial collapse in 2011.

The likely answer is that Turkey drew on vast amounts of credit from Saudi and other Gulf state banks, with strategic as well as financial motives. Data from the Bank for International Settlements show that Turkey financed a large part of its enormous deficit through the interbank market, that is, through short-term loans to Turkish banks from other banks.

Western banks report no such exposure to Turkey; the Gulf banks do not report regional exposure, and anecdotal evidence suggests that Sunni solidarity had something to do with the Gulf states’ willingness to take on Turkish exposure.

Relations between Turkey and the Gulf States are now in shambles. Saudi Arabia abhors the Muslim Brotherhood, which wants to replace the old Arab monarchies with Islamist regimes founded on modern totalitarian parties, while Erdogan embraced the Brotherhood. The Saudis are the main source of financial support for Egypt’s military government, while Ankara has denounced the military’s suppression of the Muslim Brotherhood.

Whether the Gulf States simply ran out of patience or resources to support Erdogan’s credit binge, or whether their displeasure at Turkey’s misbehavior persuaded them to withdraw support, is hard to discern. Both factors probably were at work. In either case, Erdogan’s rancor at Saudi Arabia has brought him closer to Teheran.

Turkey should have restricted credit growth and raised interest rates to reduce its current account deficit while it still had time. Erdogan, though, did the opposite: Turkish banks increased their rate of lending while reducing interest rates to businesses and consumers.

Given the country’s enormous current account deficit, this constituted irresponsibility in the extreme. Erdogan evidently thought that his mandate depended on cheap and abundant credit. The credit bubble fed construction, where employment nearly doubled between 2009 and 2013. Construction jobs increased through 2013, after manufacturing and retail employment already had begun to shrink.

Source: Central Bank of Turkey

I predicted the end of Erdogan’s supposed economic miracle in the Winter 2012 edition of Middle East Quarterly, comparing Erdogan’s boomlet to the Latin American blowouts of the 1990s:

In some respects, Erdogan’s bubble recalls the experiences of Argentina in 2000 and Mexico in 1994 where surging external debt produced short-lived bubbles of prosperity, followed by currency devaluations and deep slumps. Both Latin American governments bought popularity by providing cheap consumer credit as did Erdogan in the months leading up to the June 2011 national election. Argentina defaulted on its $132 billion public debt, and its economy contracted by 10 percent in real terms in 2002. Mexico ran a current account deficit equal to 8 percent of GDP in 1993, framing the 1994 peso devaluation and a subsequent 10 percent decline in consumption.

Source: BIS

In the meantime, Turkey has entered a perfect storm. As its currency plunges, import costs soar, which means that a current account of 8% of GDP will shortly turn into 10% to 12% of GDP – unless the country stops importing, which means a drastic fall in economic activity. As its currency falls, its cost of borrowing jumps, which means that the cost of servicing existing debt will compound its current financing requirements. The only cure for Erdogan’s debt addiction, to borrow a phrase, is cold turkey.

The vicious cycle will end when valuations are sufficiently low and the government is sufficiently cooperative to sell assets at low prices to foreign investors, and when Turkish workers accept lower wages to produce products for export.

One might envision a viable economic future for Turkey as the terminus on the “New Silk Road” that China proposes to build across Central Asia, with high-speed rail stretching from Beijing to Istanbul. Chinese manufacturers might ship container loads of components to Turkey for assembly and transshipment to the European and Middle Eastern markets, and European as well as Asian firms might build better factors in Turkey for export to China. Contrary to conventional wisdom, Turkey’s path to Europe lies not through Brussels but through Beijing.

That is Turkey’s future, but as the old joke goes, it can’t get there from here.

Turkey has a small but highly competent professional class trained at a handful of good universities, but the Erdogan regime – the so-called “Anatolian tigers” – have disenfranchised them in favor of Third World corruption and cronyism. The secular parties that bear the faded inheritance of Kemal Ataturk lack credibility. They are tainted by years of dirty war against the Kurds, of collusion with military repression, and their own proclivity towards a paranoid form of nationalism.

Erdogan’s AKP is a patronage organization that has run out of cash and credit, and its fate is unclear. The highly influential Gulen organization has a big voice, including the Zaman media chain, but no political network on the ground.

No replacement for Erdogan stands in the wings, and the embattled prime minister will flail in all directions until the local elections on March 30.

The last thing to expect from Erdogan is a coherent policy response. On the contrary, the former Anatolian villager thrives on contradiction, the better to keep his adversaries guessing.

Turkish policy has flailed in every direction during recent weeks. Erdogan’s Iran visit reportedly focused on Syria, where Turkey has been engaged in a proxy war with Iran’s ally Basher al-Assad. Ankara’s support for Syrian rebels dominated by al-Qaeda jihadists appears to have increased; in early January Turkish police stopped a Turkish truck headed for Syria, and Turkish intelligence agents seized it from the police. Allegedly the truck contained weapons sent by the IHH Foundation, the same group that sent the Mavi Marmara to Gaza in 2010. The Turkish opposition claims that the regime is backing al-Qaeda in Syria. One can only imagine what Erdogan discussed with his Iranian hosts.

Some 4,500 Turks reportedly are fighting alongside 14,000 Chechnyans and a total of 75,000 foreign fighters on the al-Qaeda side in Syria. Ankara’s generosity to the Syrian jihadists is a threat to Russia, which has to contend with terrorists from the Caucasus, as well as Azerbaijan, where terrorists are infiltrating through Turkish territory from Syria. Russia’s generally cordial relations with Turkey were premised on Turkish help in suppressing Muslim terrorism in the Caucasus. There is a substantial Chechnyan Diaspora in Turkey, aided by Turkish Islamists, and Moscow has remonstrated with Turkey on occasion about its tolerance or even encouragement of Caucasian terrorists.

I doubt that Erdogan has any grand plan in the back of his mind. On the contrary: having attempted to manipulate everyone in the region, he has no friends left. But he is in a tight spot, and in full paranoid fury about perceived plots against him. The likelihood is that he will lean increasingly on his own hard core, that is, the most extreme elements in his own movement.

Erdogan has been in what might be called a pre-apocalyptic mood for some time. The long term has looked grim for some time, on demographic grounds: a generation from now, half of all military-age men in Turkey will hail from homes where Kurdish is the first language. “If we continue the existing [fertility] trend, 2038 will mark disaster for us,” he warned in a May 10, 2010, speech reported by the Daily Zaman.

But disaster already has arrived. In some ways Turkey’s decline is more dangerous than the Syrian civil war, or the low-intensity civil conflict in Iraq or Egypt. Turkey held the North Atlantic Treaty Organization’s eastern flank for more than six decades, and all parties in the region – including Russia – counted on Turkey to help maintain regional stability. Turkey no longer contributes to crisis management. It is another crisis to be managed.

David P. Goldman is Senior Fellow at the London Center for Policy Research and Associate Fellow at the Middle East Forum.

Related Topics: Turkey and Turks | David P. Goldman